India’s clean energy achievement over the past decade is extraordinary. From a country almost entirely dependent on coal, India today has over 275 gigawatts (GW) of renewable power (solar, wind and hydro combined), effectively making it one of the top three clean energy producers on the planet. The once-ambitious target of 500 gigawatts by 2030 now looks like it might actually happen. But this is where the real problem begins.

Sunlight peaks at noon. Energy demand peaks around 7.00 p.m. This five-to-six-hour gap between the moment the power arrives and the moment it is needed requires storage. It needs batteries that charge up during the day and empty out in the evening, bridging the difference between when nature offers power and when people actually need it.

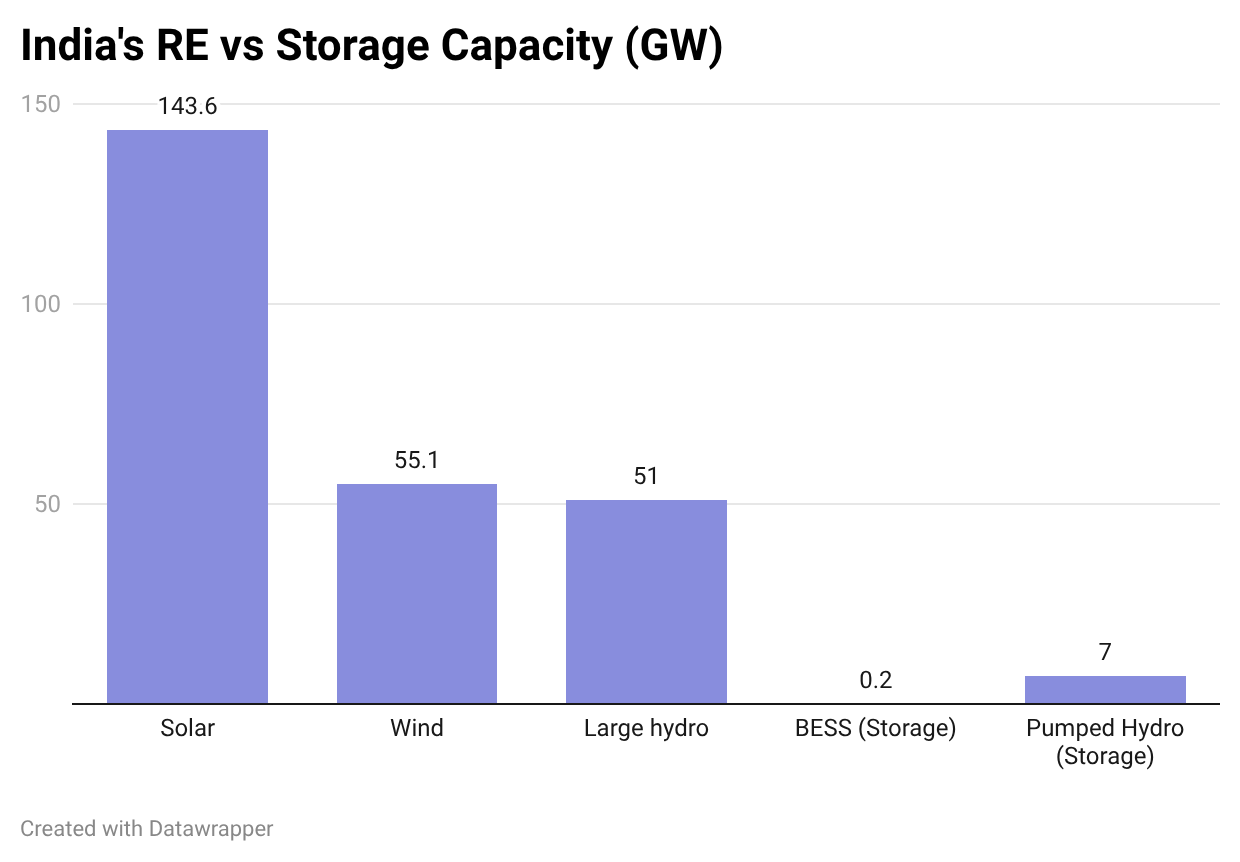

India has 275 gigawatts of total renewable capacity. But, it has only 0.2 gigawatts of battery storage. (A gigawatt of power can supply electricity to roughly 700,000 average Indian homes simultaneously.)

Figure 1. Infographics by REConnect Energy. Source: Ministry of New and Renewable Energy (MNRE).

Think of it this way. India has built one of the world’s largest and most sophisticated factories for making clean energy. And it has equipped that factory with roughly a cupboard’s worth of warehouse space. Anything the factory produces that cannot be sold immediately after leaving the production floor is simply discarded.

The price of doing nothing

Look at what actually happens to electricity prices on a sunny day in India.

- At noon when solar is flooding the grid, the price of a unit of power crashes to almost nothing, sometimes near zero rupees a unit.

- By 8.00 p.m., when the sun has set and demand has peaked, that same unit can fetch anywhere between Rs. 5 and 10 – a gap that on peak days exceeds Rs. 9 per unit. This gap exists every single sunny day.

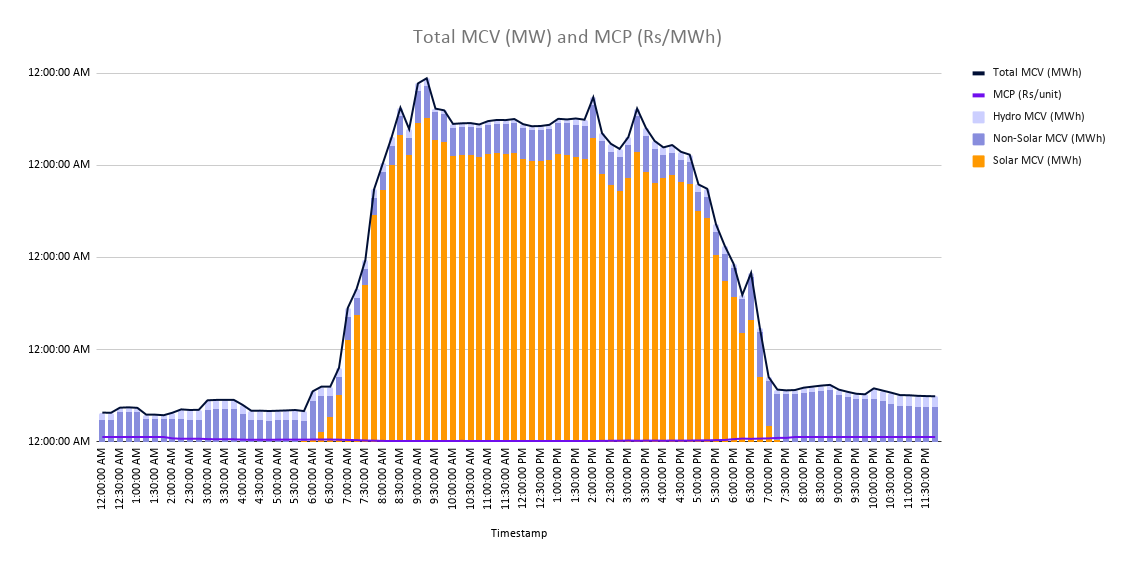

The figure below represents the market clearing value (the total amount of electricity successfully bought and sold in a specific market session or time block) and the market clearing price (the price at which it is traded).

Infographics by REConnect Energy. Source: India Energy Exchange (IEX) — GDAM Market Data, FY2024–25. Total quantum. The chart shows price patterns on typical high-solar day.

This gap is a flashing signal: whoever can store cheap electricity from noon (off peak) and sell it during the evening peak, whether it is a solar developer with Battery Energy Storage Systems (BESS) or a merchant storage plant, stands to earn the difference. CERC’s evolving regulations are making it possible. The government now requires big solar projects to come bundled with batteries, and for projects where the numbers still do not add up, it steps in with Viability Gap Funding (VGF), i.e. the cost to bridge the gap between building cost and market return.

The figure below shows the amount of electricity purchased and the price paid for it on a typical high-solar day.

Infographics by REConnect. Source: India Energy Exchange (IEX) – GDAM Market Data, FY2024–25. Solar specific. The chart shows price patterns on a typical high-solar day.

That is exactly what grid-scale batteries do. The economics already exists. The infrastructure does not.

What throwing it away actually costs

Between May and December 2025, India discarded approximately 2.3 terawatt-hours of solar electricity – power that had to be switched off because the grid couldn’t absorb it. At a conservative market price, that is around Rs. 690 crores worth of clean energy written off in just seven months.

On top of that, India’s grid rules require compensation to be paid to solar plants that are told to shut down, so the country ends up paying for power it never uses.

And the problem compounds every year. With more and more solar being added but almost no new storage to match it, the bill only grows. The table below shows three possible future scenarios. In the worst case of no new storage, India could be writing off nearly Rs. 2,000 crore of clean energy every year by 2030. In the best case where storage is built at the scale the grid actually needs, that figure falls to under Rs. 300 crore and keeps dropping.

What India could save with battery storage (illustrative estimates from IEX day ahead market, 2024-25)

| Table: Storage scenarios and their impact on renewable curtailment and revenue | |||

|---|---|---|---|

| Scenario | Annual Curtailment* (Renewable energy curtailed) |

Revenue Lost (@ Rs. 3/unit) |

TRAS** Compensation (Trend / Level) |

| Tier 1: No new storage (2030) | ~6-8 TWh* / year | ~Rs. 1,800-2,400 crore | Rising (uncapped) |

| Tier 2: 3-5 GW BESS** by 2027 | ~3-4 TWh / year | ~Rs. 900-1,200 crore | Stable / High |

| Tier 3: 47 GW BESS by 2032 | <1 TWh / year | <Rs. 300 crore | Declining |

Notes:

* TWh = Terawatt-hour; assumes Rs. 3 per unit (kWh) average power purchase cost.

** BESS = Battery Energy Storage System.

*** TRAS = Thermal Replacement Avoidance Savings (estimated compensation for avoided thermal generation).

Storage requirement targets from CEA National Electricity Plan 2022-23

Curtailment: The instruction issued by a grid operator (such as a State or Regional Load Dispatch Centre) to a power plant to reduce or stop generating electricity, typically because the transmission network cannot safely absorb what is being produced. For renewable plants, curtailment means permanently wasted clean generation – the wind or sunlight passes without producing usable electricity.

TRAS (Tertiary Reserve Ancillary Service): Manually activated generation adjustments called upon by system operators to balance supply and demand. When a renewable energy plant is instructed to curtail output for grid security reasons, regulations from the Central Electricity Regulatory Commission (CERC) entitle the generator to compensation; commonly referred to as TRAS compensation – typically calculated as a percentage of contracted power purchase tariff per unit of electricity lost.

Terawatt-hour (TWh): Roughly equivalent to the annual electricity consumption of around 85,000-90,000 average Indian households.

BESS (Battery Energy Storage System): Large-scale batteries connected directly to the electricity grid. Unlike household batteries, grid-scale BESS units are engineered to absorb surplus electricity during periods of excess generation and release it during periods of peak demand. They are typically measured in megawatts (power output) and megawatt-hours (total energy stored).

The choice between these future scenarios is not a technical one, rather a policy one.

The good news: We know what to do

India’s national electricity planners have already worked out what the grid needs. By 2032, to run reliably on predominantly renewable power, the country will need around 47GW of battery storage and 27GW of pumped hydro. The latter is a technology that stores energy by pumping water uphill when electricity is abundant, then releasing it through turbines when it is scarce.

Today, India is a fraction of the way there. But the distance between here and there is not a mystery – we have a set of specific, fixable problems, and we know how to fix them.

Infographics by REConnect Energy. Source: CEA National Electricity Plan 2022-23. The first fix is letting storage earn properly. Right now, a battery project typically has to choose either to store and sell power, or provide grid-balancing services, but rarely both at once.

A shop that could only serve walk-in customers or delivery, never both, would struggle too. Unlocking all revenue streams simultaneously would make the economics work and bring private investment in at the scale needed.

The second is signing the contracts. India has auctioned enormous amounts of storage capacity on paper. But as of late 2025, projects worth around 44 gigawatts of RE were still waiting for the formal agreements that allow them to move from auction to construction. Every month of hesitation is a month of storage that doesn’t get built.

The third is treating storage as infrastructure, not a pilot project. India doesn’t build roads one experiment at a time. Storage, which is just as essential to a renewable grid as roads are to a city, deserves the same commitment: planned at scale, integrated from the start, and not bolted on as an afterthought.

And here is the really encouraging part: the cost of storage has already collapsed. Just three years ago, building a grid battery in India cost around Rs. 10 per unit of electricity stored. Today it is closer to Rs. 2.8 with the expectation that BESS will be utilised for 1.5 cycles per day. A cycle means the battery charges once and discharges once; 1.5 cycles a day means it is doing that job more than once every single day. The technology got dramatically cheaper while the policy conversation was still catching up.

Infographics by REConnect Energy. Source: CEA National Electricity Plan 2022-23.

The market is moving. The technology is ready. The window to get the policy right is still open but it will not stay open indefinitely.

The second chapter of the energy transition

For a decade, India’s energy story was about how many gigawatts it could install. That chapter has been written, and it is a good one.

The next chapter is about something harder and less visible: timing. Making sure that the power India generates is actually available when people need it. That the solar surge at noon translates into lit homes and running fans at 7.00 p.m.; not into power cuts.

REConnect Energy is building AI-first digital infrastructure for the future of energy. The company helps renewable energy developers, grid operators, utilities, traders, industrial consumers, and EV ecosystem players manage growing grid complexity with greater intelligence, accuracy and reliability. Through digital platforms and grid-integrated hardware, REConnect Energy supports smarter grid operations, better forecasting, and a more resilient, data-driven energy ecosystem for India and beyond.