A recent study estimates that the global transition to net zero by 2050 will require $275 trillion in investment in physical assets – or $9.2 trillion annually. A big chunk of that money is expected to come from private financial institutions. Commercial banks alone may need to support $2.0-2.6 trillion annually.

This shift is already happening. The global sustainable finance market reached $13.4 trillion in 2025 and could cross $27 trillion by 2031.

For companies, this changes the rules of finance. Today, investors and lenders are not looking only at balance sheets. They are also looking at emissions data, climate targets, governance standards and sustainability performance before deciding who gets capital and at what cost.

That means your next loan, bond or refinancing could depend as much on your ESG data as on your profits.

For decades, climate change sat mostly in sustainability reports and CSR presentations. Today, it is moving directly into balance sheets, loan agreements and investment decisions. A company’s emissions profile is increasingly treated as a financial risk indicator, much like debt levels or cash flow stability.

That shift is changing what gets funded in the real economy. Solar parks, electric mobility, battery manufacturing and green buildings are attracting large pools of capital globally, while high-emission sectors are facing growing pressure to prove they can transition.

So first, what exactly is sustainable finance?

What is sustainable finance?

Sustainable finance refers to investments and financial products that include environmental, social and governance (ESG) factors in decision-making.

One way to understand sustainable finance is to follow the money. Investors and banks raise capital from markets specifically for sustainability-aligned purposes, channel it into sustainability-linked financial products, and companies then use that money to build projects in the real world, from renewable energy plants and electric bus fleets to low-carbon industrial upgrades and water recycling systems.

In practice, it mainly appears in four forms:

• Green Bonds and Loans: Money is used only for environmental projects such as renewable energy, energy efficiency, clean transport and water management.

• Sustainability-Linked Bonds and Loans (SLBs/SLLs): Interest rates go up or down depending on whether a company meets agreed sustainability goals, usually linked to your Scope 1 and 2 emissions reduction targets.

• Transition Finance: Funding meant for high-polluting industries such as steel, cement, chemicals, aviation and shipping to help them reduce emissions over time.

• ESG-aligned Equity and Funds: Investment funds that choose companies based on ESG standards and sustainability performance, increasingly governed by frameworks like SFDR in Europe.

In India, this transition is already visible. Companies such as Tata Steel and ReNew have raised sustainability-linked financing tied to climate and energy goals, while lenders are increasingly building ESG-linked conditions into large financing arrangements.

All of these depend on one thing: reliable and verifiable ESG data.

Without strong emissions data, transition plans and sustainability reporting, companies may struggle to raise funds through these instruments, attract investors or secure better financing terms.

This is where many companies struggle. Investors increasingly want emissions data that can be independently verified and compared across industries and countries. That has turned ESG reporting from a branding exercise into a financial requirement.

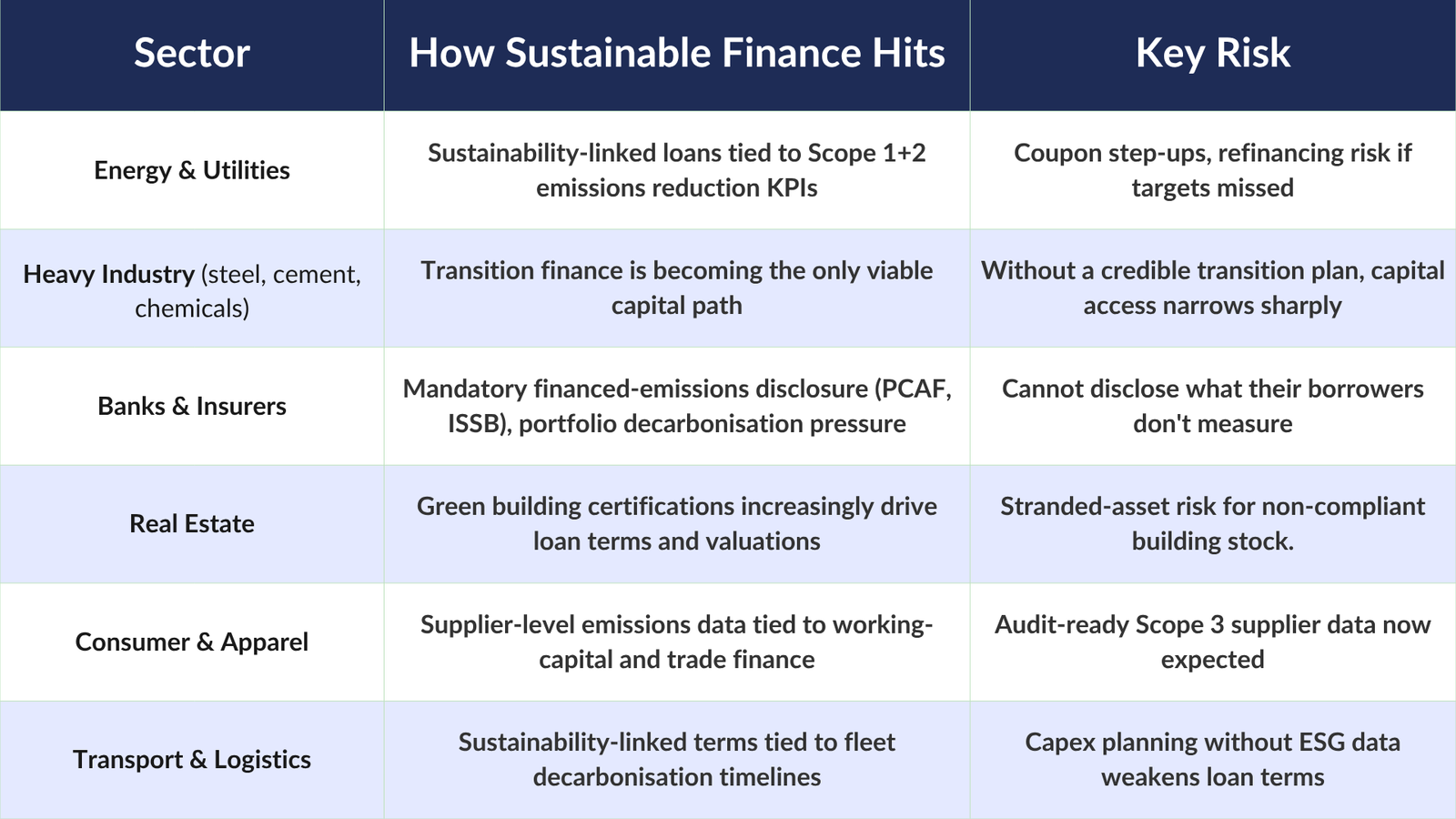

Which sectors are most affected?

Industries that use large amounts of capital, produce high emissions or face close scrutiny from lenders are most exposed.

See the table below.

Infographics courtesy Oren

The bottom line is simple: Companies without audit-ready ESG data may slowly lose access to the cheapest sources of capital, often without realising it until refinancing becomes more expensive.

Not all sustainable finance is automatically sustainable, however. Around the world, regulators are also cracking down on greenwashing, where companies or funds exaggerate environmental claims without meaningful action behind them. That is one reason disclosure standards, third-party assurance and climate reporting rules are becoming stricter.

GIFT City, RBI and BRSR connection

India’s sustainable finance ecosystem has evolved quickly. Three major developments are shaping the space:

First, GIFT City’s Sustainable Finance Hub: This gives Indian companies a domestic route to access sustainable capital markets that were earlier available mainly offshore.

Second, RBI’s Green Deposits Framework: Banks accepting green deposits now have to direct funds toward approved green activities, increasing pressure for better reporting and transparency.

Third, SEBI’s BRSR Core framework: Mandatory sustainability disclosures and assurance requirements are helping Indian firms build the reporting systems global investors increasingly expect.

For Indian companies, this matters beyond compliance. Stronger sustainability disclosures can improve access to global investors, especially as European and international financial institutions tighten ESG expectations across supply chains and investment portfolios.

What should your organisation do?

Becoming sustainable-finance ready is no longer just a sustainability exercise. It requires companies to treat climate data, transition planning and ESG disclosures with the same seriousness as financial reporting.

In practice, the strongest organisations are focusing on six priorities:

They build a cross-functional leadership team, where the finance, sustainability, risk and operations teams work together instead of operating in silos. Next, they assess their current ESG data quality – how the company measures emissions, tracks sustainability metrics and reports disclosures – to identify gaps. These could be in accuracy, governance and verification.

Parallelly, they examine existing loans, bonds and investor relationships to see where ESG-linked conditions or sustainability expectations already apply.

Next, they create a credible transition plan. Investors increasingly want detailed roadmaps with clear timelines, spending plans and accountability, not just long-term climate promises. Reporting systems are upgraded accordingly. Spreadsheet-based reporting is becoming difficult to defend, and companies are increasingly investing in dedicated ESG data and disclosure platforms.

Finally, they start conversations with investors early. The best time to discuss sustainability goals with lenders and investors is before refinancing or fundraising discussions begin.

The companies moving fastest are not necessarily the greenest. They are often the ones building the clearest systems for measuring, reporting and improving sustainability performance.

Are you sustainable-finance ready? A checklist

Here are seven questions every Chief Finance Officer should be able to answer in 2026:

• Do you know which of your loans or bonds include ESG-linked targets or penalties?

• Are your Scope 1 and Scope 2 emissions measured using recognised standards such as the GHG Protocol?

• Have you calculated how your ESG profile affects your borrowing costs compared to competitors?

• Does your transition plan include realistic milestones, spending plans and governance structures?

• Have you identified which sustainable finance products your company could access in the next 12-24 months?

• Are your finance and sustainability teams working from the same set of data?

• Does your board review ESG metrics as seriously as financial performance?

This explainer is based on research by Oren, an agentic AI platform for GHG accounting, sustainability reporting, supply chain sustainability, climate risk and sustainable finance.